It’s a well-documented issue in the Australian economy. According to the Australian Small Business and Family Enterprise Ombudsman, small businesses are often forced to act as financiers for larger companies due to persistently late payments. This isn’t just an accounting headache; it’s a domino effect that can destabilise an entire business.

When a major client in Sydney or a construction project in Perth pays 60 days late, the impact cascades through the supply chain. That single delay means a tradie in Melbourne might struggle to pay their apprentice on time. A retailer in Brisbane can’t restock their shelves for the weekend rush. A small manufacturer is left unable to pay for essential raw materials. This is one of the most significant SME cash flow challenges Australia faces.

From your perspective as a business owner, the situation is even more direct. Every day you wait for an invoice to be paid, you are effectively acting as an interest-free bank for your customers. You are funding their operations with your own working capital while your cash flow slowly dries up. This creates immense pressure, from the constant worry about meeting payroll and rent to the inability to seize new opportunities because your funds are tied up.

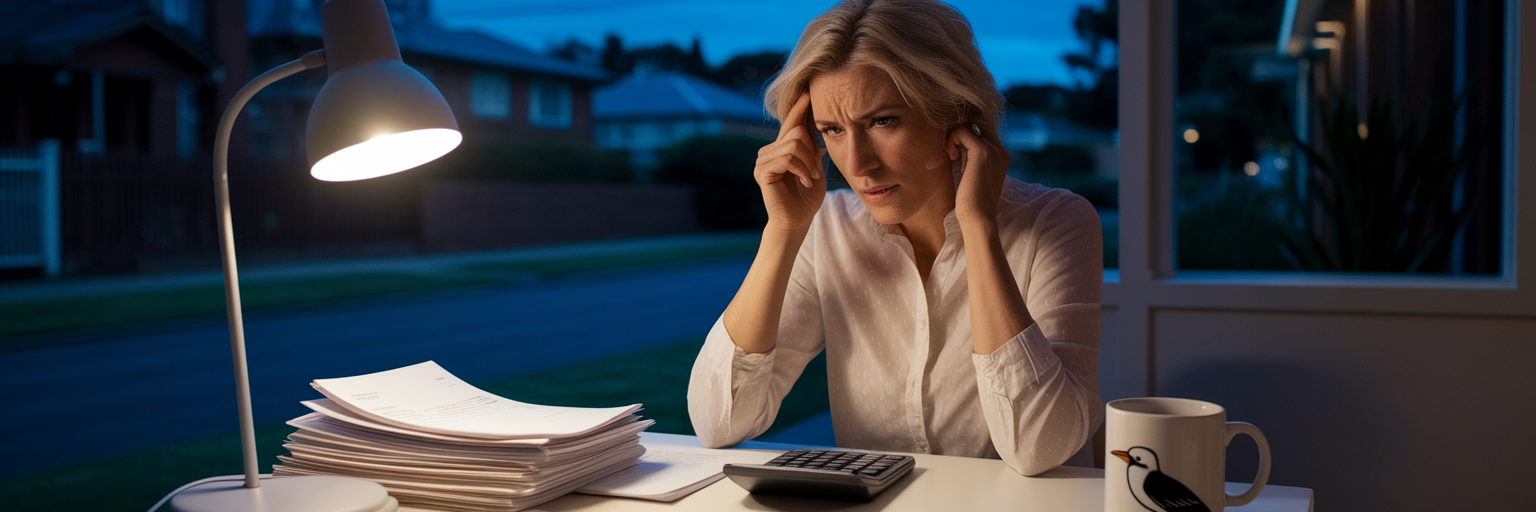

The most obvious cost of a late payment is the missing money itself. But the true damage runs much deeper, creating secondary costs that quietly drain your resources and momentum. The administrative burden alone is staggering. Some industry data suggests Australian business owners can spend nearly two full weeks a year just chasing overdue invoices. Think about that. That’s time you could have spent quoting new jobs, training your team, or simply taking a well-earned break.

This lost time could be reinvested into the business, a topic we explore further in our resources for SME growth. Beyond the clock, there’s the strain on crucial business relationships. When you can’t pay your own suppliers because you’re waiting on a client, it can damage your reputation and jeopardise the favourable terms you’ve worked hard to secure. For tradies relying on materials or retailers needing stock, a breakdown in the supply chain is a critical risk.

Perhaps the most dangerous hidden cost is being pushed into using high-interest, last-resort options to cover immediate expenses. Turning to personal credit cards or expensive overdrafts to pay for business costs can initiate a damaging debt cycle that becomes increasingly difficult to escape. These stop-gap measures often come with punishing interest rates and fees, turning a temporary cash flow problem into a long-term financial burden. Understanding how to manage business cash flow means recognising these hidden threats before they escalate.

| Cost Category | Description | Estimated Financial Impact |

|---|---|---|

| Administrative Labour | Time spent by owner/staff on calls, emails, and follow-ups (e.g., 5 hours @ $50/hr) | $250 |

| Opportunity Cost | Value of new business that could have been won in that time | $500 – $1,500+ |

| Stop-Gap Finance | Interest on a credit card or overdraft used to cover expenses for 30 days | $150 – $300 |

| Supplier Relationship Damage | Potential loss of early payment discounts or favourable terms | Intangible but significant |

| Total Hidden Cost | Beyond the initial $10,000 invoice amount | $900 – $2,050+ |

Note: These figures are estimates based on average hourly rates and standard credit card interest. The opportunity cost can vary significantly but highlights the value of time lost to chasing payments instead of focusing on business growth.

When you’re facing an urgent cash flow gap, the last thing you have is time. Yet, the slow, cumbersome process of applying for a traditional bank loan is completely out of sync with this reality. Waiting weeks, or even months, for an approval simply doesn’t work when payroll is due on Friday or a key supplier needs payment today. The traditional finance system wasn’t built to provide effective late payment solutions for business in a dynamic economy.

Many healthy, thriving Aussie SMEs find themselves automatically excluded by rigid eligibility criteria. Common barriers include:

This leaves countless viable businesses without support precisely when they need it most. The system is fundamentally misaligned with the speed and flexibility that modern Australian businesses require to operate effectively.

Instead of a last resort, a short-term business loan should be seen as a strategic tool for proactive financial management. It’s about bridging the gap between invoicing a client and getting paid, ensuring your business never loses momentum. This modern approach to finance is built on three key pillars.

The primary advantage of modern lenders is speed. When an unexpected bill arrives or a client payment is delayed, you need a solution that moves at the speed of your business. With tech-driven platforms like ours, you can get access to fast business finance for invoices, often with same-day approval and funding. This immediate relief allows you to cover urgent costs without hesitation and keep your operations running smoothly.

We believe your business should be assessed on its current health and potential, not just its history. Our streamlined digital application eliminates the need for mountains of paperwork. We look at your recent performance, which means finance becomes accessible even if you have challenges that banks see as deal-breakers. This approach means that even a strong business with a history of financial difficulty can secure a bad credit business loan to move forward and grow.

No two businesses are the same, so your funding shouldn’t be one-size-fits-all. Flexible finance can be tailored to your specific needs, whether you need a small amount to cover a single late invoice or a larger sum to improve business working capital. Features like the option for up to six months of zero repayments are designed to directly support your cash flow, giving you breathing room to stabilise and plan ahead. To see how a flexible loan could be tailored to your specific circumstances, you can start the simple process online.

Aussie SMEs no longer have to be at the mercy of their clients’ payment schedules. Waiting for invoices to be paid shouldn’t dictate your ability to operate and grow. By leveraging fast and flexible short term business loans Australia, proactive owners can stop the domino effect before it even starts. This is about making an empowering choice to maintain control over your financial destiny, ensuring you have the working capital to thrive, not just survive. Take the first step towards financial control and explore how modern funding can support your business journey.